Dreaming of Your First Home in Christchurch? Unlock Your Options!

For first-home buyers (FHB) in Christchurch, understanding your financial support options is key. The good news is, tools like KiwiSaver withdrawals and government-backed First Home Loans can make owning a new build more achievable than ever.

This practical guide will quickly break down how these crucial schemes work, helping you navigate your path to a new Townhouse in Wigram.

Your KiwiSaver: Unlocking Your Deposit

Your KiwiSaver account is likely your most significant deposit contributor. Here’s what you need to know:

- Eligibility Essentials:

- First-Time Buyer: You must be a genuine first-home buyer or qualify for a ‘second-chance’ withdrawal.

- NZ Resident: A NZ citizen or permanent resident.

- 3+ Years Contribution: Must have contributed to KiwiSaver for at least three years.

- Occupy the Home: You must intend to live in the home for at least six months.

- How Much Can You Withdraw?

- You can withdraw all your contributions (personal, employer, and government) except for the initial $1,000.

- The Process (Simplified):

- Pre-Approval: Get a pre-approval letter from your KiwiSaver provider before signing a sale agreement.

- Lawyer’s Role: Your lawyer handles the final application, ensuring funds are ready for settlement (allow 10-15 working days before settlement).

- New Build Flexibility: For Turnkey Townhouses, withdrawals can often be structured to align with staged payments or final settlement.

Government Support: First Home Loan & Grant

These Kāinga Ora initiatives are designed to boost your purchasing power.

- First Home Grant (The Cash Boost)

This is a direct payment from the government towards your deposit:

- For New Builds: You can receive up to $5,000 as an individual or $10,000 as a couple.

- Key Eligibility:

- KiwiSaver has contributed for 3+ years.

- Income Caps: Single earner up to $95,000; two or more earners up to $150,000.

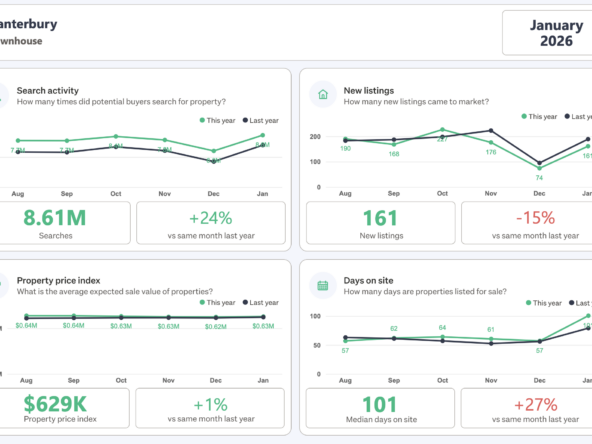

- Christchurch Price Cap (Crucial for You!): For new buildings in Canterbury, the current house price cap is $700,000.

- Good News! Tailored Homes’ Wigram project, priced from $617k, comfortably fits this cap.

- First Home Loan (Low Deposit Mortgage)

This loan, guaranteed by Kāinga Ora, is a game-changer if you have limited savings:

- 5% Deposit: It allows banks to lend with as little as a 5% deposit, as the loan is backed by Kāinga Ora.

- LVR Exemption: Crucially, this type of loan (especially for new builds) is often exempt from standard LVR restrictions, making it easier for banks to approve.

- Eligibility: Similar income and residency criteria as the Grant.

- Cost: A Kāinga Ora ‘Lender’s Mortgage Insurance’ fee (typically 1% of the loan value) applies.

Your Smart Path to a New Build in Wigram

Navigating these options can seem complex, but it doesn’t have to be.

- Engage a Mortgage Broker: They are often free for you and act as invaluable guides, knowing each bank’s specific criteria and streamlining your application process.

- Plan Ahead: Ensure all applications (KiwiSaver, Grant) are submitted with ample time before settlement.

With the support of KiwiSaver and government schemes, combined with the clear advantages of a new build, your dream of owning a New Turnkey Townhouse in Tailored Homes’ Wigram project is within reach.

Ready to explore your tailored finance options for a Wigram Turnkey Townhouse?

➡️ Next Step: Get Your Free Eligibility Assessment!

Click below to connect with our recommended mortgage brokers, who specialise in new build financing and can assess your exact eligibility for KiwiSaver withdrawals, First Home Loans, and Grants.